The Income-Tax Bill, 2025, introduces a new ‘Tax Year’ concept, replacing the existing Assessment Year, aiming to simplify tax reporting.

About Income-Tax Bill, 2025

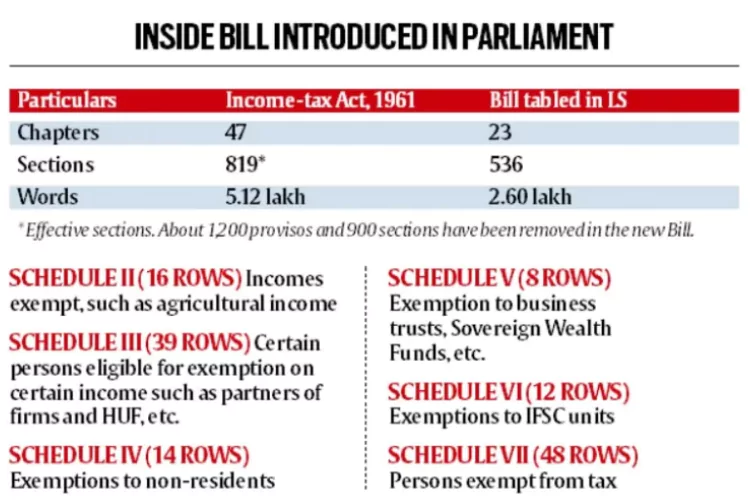

- Simplification: Streamline the 1961 Income-tax Act by removing obsolete provisions, redundant clauses, and complex legal jargon.

- Modernization: Reflect evolving economic realities (e.g., digital assets, new income sources).

Key Features of the Bill

- Tax Year: A 12-month period starting from April 1, during which income will be assessed and taxed in the same financial year.

- No change in the Financial Year (FY): It will continue to start on April 1 and end on March 31.

- Calendar Year Not Adopted: The new bill does not align with the calendar year for taxation purposes.

Existing System (Income-tax Act, 1961)

- Two concepts: Financial Year (FY) and Assessment Year (AY)

- Assessment Year (AY): The year following the financial year in which income is earned.

- Example: For FY 2024-25, the AY is 2025-26.

- Issue: Many taxpayers confuse FY and AY, leading to incorrect tax filings, delays in refunds, and procedural hassles.

|

- Inclusion of Virtual Digital Assets (VDAs) as Capital Assets:

- Cryptocurrencies, NFTs, and other digital assets are now formally recognized as capital assets.

- Taxation: Treated similarly to traditional assets like land, buildings, shares, securities, bullion, jewelry, and artwork.

- Implications: Ensures clarity on taxation of digital assets, aligning with global trends and addressing the growing digital economy.

- Expanded Definition of “Virtual Digital Space”: Taxpayers under investigation must provide access to their digital records, including email servers, social media accounts, online investments, trading and banking accounts, cloud servers, and digital platforms.

- Current Practice: Tax authorities already demand access to laptops, hard drives, and emails during surveys, searches, and seizures.

- Capital Gain Exemptions: Section 54E of the Act, which details exemptions for capital gains on transfer of capital assets prior to April 1992 has been removed in the Bill.

- Deductions have been streamlined, and outdated exemptions removed.

- Dispute Resolution:

- Dispute Resolution Panel (DRP): Clearer guidelines for issuing decisions, reducing ambiguity and potential litigation.

- Income and Tax Rates:

- Expands the definition of income to encompass emerging sources.

- Provides detailed tables for exempt income, conditions for claiming exemptions, deductions, TDS, and TCS in separate schedules for enhanced clarity.

- New Tax Regime: Slabs provided in tables; old regime rates omitted, signaling a shift toward promoting the new regime.

- Continuity: No major changes in tax structure, penalties, or compliance rules.

Key Implications

- Reduced Litigation: Simplified language and consolidated provisions may minimize interpretational disputes.

- Ease of Compliance: Tables and streamlined sections enhance taxpayer understanding.

- Digital Economy Integration: Recognition of VDAs and digital income sources aligns tax laws with modern economic trends.

- Stability: Maintains existing tax structure to avoid disruption while modernizing procedural aspects.

Criticisms/Challenges

- Lack of Penalty Reforms: No major updates to penalty or compliance mechanisms, potentially missing an opportunity to improve enforcement.

- Old Tax Regime Ambiguity: Exclusion of old regime slabs from the Bill raises questions about its future.

- Privacy & Surveillance: Possible infringement on individuals’ digital privacy.

- Need for Safeguards: Clear guidelines required to protect taxpayer rights from excessive scrutiny.

- Administrative Efficiency: Aims to streamline tax collection and reduce legal disputes.

Legislative Process

- Parliamentary Review: Bill referred to a Parliamentary Committee; amendments likely before implementation.

- Effective Date: Likely April 1, 2026, post-presidential assent.

Historical Context

- Past Reforms:

- Direct Taxes Code (DTC), 2010: Lapsed with the 15th Lok Sabha.

- 2018 Task Force: Drafted a new law but not implemented.

- Philosophical Shift: Aligns with “Nyaya” (justice) ethos, similar to recent criminal code reforms.

14 Feb 2025

14 Feb 2025

GS Foundation

GS Foundation Crash Course

Crash Course Combo

Combo Optional Courses

Optional Courses Degree Program

Degree Program