Books & Magazines

UPSC CSE : 2013

Answer:

| Approach:

Introduction:

Body

Conclusion

|

Introduction:

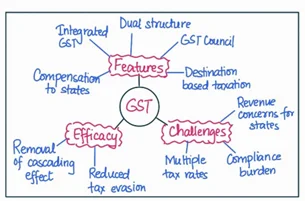

Goods and Services Tax (GST) is an indirect, comprehensive, multi-stage, destination-based tax that is levied on every value addition. GST replaced a host of indirect taxes being levied by the central and state governments, which has changed the taxation landscape.

Body:

Rationale behind GST:

Thus, Goods and services tax was proposed to subsume all indirect taxes at central and state level, with two uniform rates, viz central GST and State GST.

The reasons for delay in its rollout were:

Conclusion:

GST has been a significant reform which eliminates cascading of taxes and reduces transactional and operational costs, thereby enhancing the ease of doing business and catalyzing the “Make in India” campaign. There have been concerns, but the system continues to evolve. Therefore, GST is going to be a game changer for our economic growth and employment generation in the long run.

Books & Magazines

Books & Magazines

Prelims Wallah (Q&A Bank)

Udaan

Udaan 500+

Budget & Economic Survey

Monthly Current Wallah

Weekly Current Wallah

Editorial Summary

Editorial Q&A Compilation

NCERT Wallah

Prahaar (Mains Wallah)

Marks Booster

Mains Wallah (Q&A Bank)

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Crash Course

Crash Course Combo

Combo Optional Courses

Optional Courses Degree Program

Degree Program