Books & Magazines

UPSC CSE : 2017

Answer:

| Approach:

Introduction:

Body

Conclusion

|

Introduction:

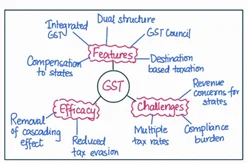

The Constitution (One Hundred and First Amendment) Act, 2016, introduced the Goods and Services Tax (GST) in India, a comprehensive indirect tax system aimed at streamlining the taxation process and creating a common national market for goods and services.

Body:

The amendment’s salient features include:

The efficacy of the GST in removing the cascading effect of taxes and providing a common national market for goods and services can be assessed as follows:

However, there are some concerns and challenges:

Conclusion:

Addressing the challenges faced by businesses and states, and further simplifying the tax structure, can enhance the overall efficacy of the GST system.

Books & Magazines

Books & Magazines

Prelims Wallah (Q&A Bank)

Udaan

Udaan 500+

Budget & Economic Survey

Monthly Current Wallah

Weekly Current Wallah

Editorial Summary

Editorial Q&A Compilation

NCERT Wallah

Prahaar (Mains Wallah)

Marks Booster

Mains Wallah (Q&A Bank)

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Crash Course

Crash Course Combo

Combo Optional Courses

Optional Courses Degree Program

Degree Program