The Government of India has launched EASE 8.0 (Enhanced Access and Service Excellence) as the latest phase of reforms to strengthen Public Sector Banks (PSBs) through digital transformation, improved risk management, and enhanced customer service.

- The EASE Reform Agenda is finalised on yearly basis at the start of each financial year (FY), under the guidance of EASE Steering Committee of member PSBs under the aegis of Indian Banks’ Association.

About EASE 8.0

- EASE₹ise/ The EASE 8.0 reform agenda focuses on Gen-AI and Agentic AI adoption, inclusive banking, sustainability, improved customer experience, and operational efficiency to make Public Sector Banks agile, future-ready, and customer-centric.

What is EASE (Enhanced Access and Service Excellence)?

- EASE is a reform programme launched in 2018 by the Department of Financial Services (DFS), Ministry of Finance, in collaboration with the Indian Banks’ Association and authored by Boston Consulting Group.

- Objective: To improve the performance, governance, and customer orientation of public sector banks.

- Under EASE Reforms, normally timelines are defined within the FY, and the metrics are scheduled for operationalisation from April onwards during the FY, to ensure structured implementation.

|

Major Initiatives introduced in EASE 8.0

- Governance:

- Inclusive Governance Framework to ensure Divyangjan’s representation in Customer Service Committees, Grievance Redressal Cell, and setting up a dedicated Accessibility Cell having Accessibility employees

- Dedicated outbound sales team governance structures

- Enhanced Learning and Development governance

- Environmental, Social and Governance Scorecard integration and dedicated Customer Retention Squad governance framework

- Artificial Intelligence roadmaps and leveraging its use cases for operational efficiency

- Customer Service:

- Specifically designed asset and liability products for Gig/platform workers, Youth, Women and Startups

- Multilingual Customer service in Regional Languages (Digital Channels and Service forms)

- Enhanced Mobile-App capabilities for Retail and Micro, Small & Medium Enterprises (MSMEs) customers

- Asset and Liability digital assisted journey for customer onboarding

- Virtual Relationship Managers for identified customers

- End-to-end digital journeys for trade finance solutions

- Self-service touch points for Divyangjans

- Digital Lending:

- Digital journeys for Retail, MSME and Agri-loan products.

- Digital assisted framework for customer convenience

- Integrating advanced capabilities in loan management system for MSME underwriting

- Integration with Account Aggregator ecosystem

- Automatic credit appraisal generation capabilities and use of analytics/AI in underwriting

- Risk Management:

- Focus on Expected Credit Loss models

- Digital portal/platforms for monitoring of Operational Risks taxonomy and Early Warning Signals

- Fraud prevention and Anti-Money Laundering checks in the existing as well as new bank customers’ onboarding journey

- Enhanced models for mule account identification and enhanced customer due diligence

- Technology Modernisation and resilience of IT Applications by setting up Resiliency Operation Centre and efficient third-party risk management

- Digital forensic readiness for cyber incidents

- App/platform/portal-based recovery and collection monitoring mechanisms

Various Stages of EASE Reforms

| EASE Version |

Key Features |

| EASE 1.0 |

Focused on improving transparency and efficiency in resolving Non-Performing Assets (NPAs) and strengthening overall performance of Public Sector Banks (PSBs). |

| EASE 2.0 |

Built on EASE 1.0 with reforms across six themes:

- Responsible Banking;

- Customer Responsiveness;

- Credit Off-take; P

- SBs as UdyamiMitra (SIDBI portal for MSME credit management);

- Financial Inclusion & Digitalisation;

- Governance and Human Resource reforms.

|

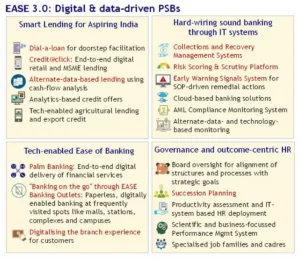

| EASE 3.0 |

|

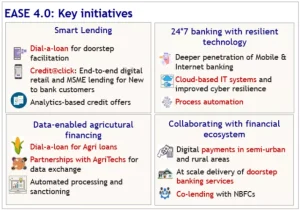

| EASE 4.0 |

|

| EASE 5.0 |

Emphasised new-age digital capabilities and inclusive banking.

Focus areas include:

- Digital customer experience

- Support to MSMEs and agriculture, and initiatives across business growth, profitability, risk management, customer service, operations, and capability building.

|

| EASE 6.0 |

Focus Areas Include:

- Delivering excellence in customer service with digital enablement

- Digital and analytics-driven business improvement

- Tech and data enabled capability building

- Developing people and enhancing HR operations

|

| EASE 7.0 |

Focus Areas Include:

- EASE 7.0 is being launched with an emphasis on enabling banks to drive national priorities, maintaining a strong customer service orientation, managing operational risks effectively and catalyzing new-age capability build.

|

Achievements of EASE Reforms

As per RBI’s provisional data, as on December 2025, below are key highlights that illustrate the significant impact witnessed by PSBs through EASE Reforms:

- Record profitability turnaround: During FY2024-25, all PSBs were profit making with the highest ever aggregate net profit of ₹1.78 lakh crore, as against the loss of ₹85,371 crore reported by PSBs in FY2017-18.

- Further, the net profit of PSBs during the first nine months of FY2025-26 was ₹1.46 lakh crore.

- Sharp decline in Gross NPA ratio: Gross NPA ratio of PSBs have declined to a fresh low of 2.10% (₹2.54 lakh crore) in Dec-25 from 4.97% (₹2.79 lakh crore) in Mar-15, and from a peak of 14.58% (₹8.96 lakh crore) in Mar-18.

- Improved Capital to Risk- weighted Assets Ratio (CRAR): Capital adequacy has improved significantly with Capital to Risk- weighted Assets Ratio (CRAR) of PSBs improving by 401 bps to reach 15.46% in Dec-25 from 11.45% in Mar-15.

- Exit from RBI’s PCA framework : During FY2024-25, no PSB was under RBI’s Prompt Corrective Action (PCA) as against FY2017-18 where 11 PSBs out of 21 were under PCA.

- Expansion of end-to-end digital journeys: In FY2024-25, all PSBs have digital journeys across Retail, Agriculture and MSME sectors, while no such journeys were offered in FY2017-18.

Limitations

- Persistent Asset Quality Concerns: Despite improvements, Non-Performing Assets (NPAs) remain a challenge in some Public Sector Banks due to legacy stressed assets and sectoral risks.

- Slow Implementation Across Banks: The pace of reforms and adoption of new initiatives has varied across PSBs, leading to uneven outcomes.

- Digital Infrastructure Gaps: Although digital banking has expanded, cybersecurity risks, digital literacy issues, and infrastructure gaps still affect effective implementation.

- Human Resource Constraints: PSBs continue to face skill gaps, limited autonomy, and slower decision-making compared to private sector banks.

Way Forward

- Cybersecurity and fraud risk management: PSBs should enhance cyber resilience through real-time fraud monitoring and stronger authentication.

- Capability building and HR reforms: PSBs should invest in role-based training and performance-linked HR systems to support digital banking and risk management

- Shared PSB digital utilities: PSBs should expand common platforms and shared services to reduce costs and improve delivery.

11 Mar 2026

11 Mar 2026

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program