The European Central Bank (ECB) is in the process of developing a digital euro. The “preparation phase” of this project began in November 2024.

Digital Euro

- Digital euro will allow people to pay directly from a digital wallet on smartphones or computers, eliminating the need for a bank or payment gateway.

- The Reserve Bank of India (RBI) is exploring collaborations with the US and the EU for the digital rupee’s development.

- India also plans to extend its partnership with the UAE for a cross-border pilot of Central Bank Digital Currency (CBDC).

Enroll now for UPSC Online Course

Key Features and Differences from Current Digital Payment Options

- Direct Issuance by ECB: Unlike other digital payment methods that rely on bank-managed systems, the digital euro would be directly issued and managed by the ECB, functioning as a digital equivalent of cash.

- Microtransactions and Cost-Effectiveness: The ECB envisions the digital euro as a cost-neutral option for processing microtransactions, which are currently costly with traditional banking fees.

- This could enable new digital business models and reduce reliance on intermediaries.

- Offline and Anonymous Transactions: The digital euro is designed to support offline payments, potentially offering a level of anonymity similar to physical cash.

- Depending on the end device, the money can be transferred via Bluetooth, a browser extension or a smartphone contact.

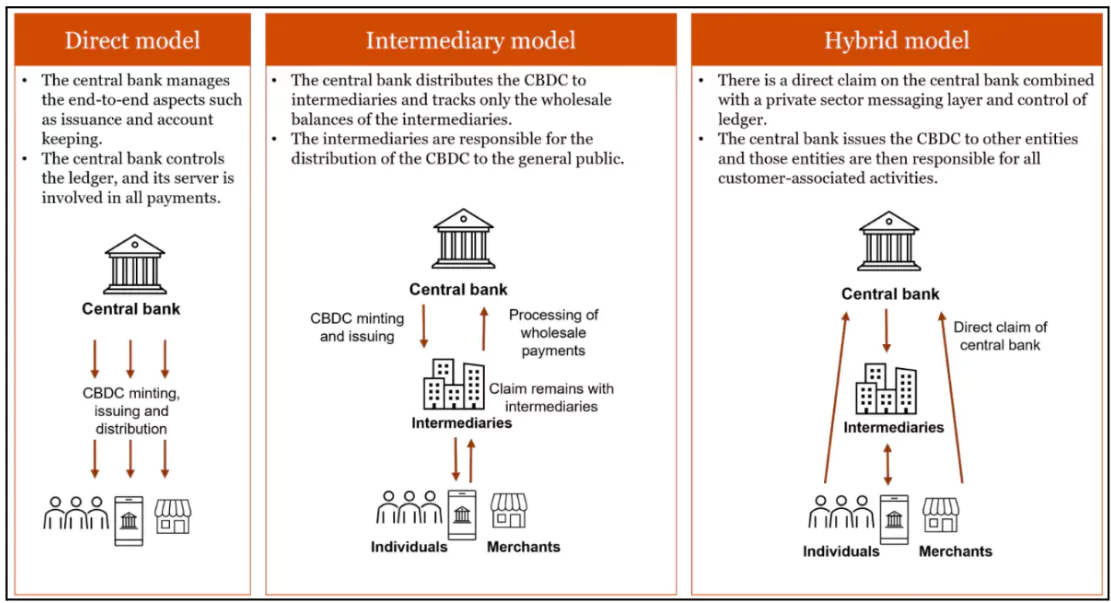

Models Of Issuance of Digital Currency

About Central Bank Digital Currency (CBDC or e-Rupee)

- It is a legal tender issued in digital form and was launched by RBI in 2022.

- Currency Type: It is equivalent to fiat currency and can be exchanged one-to-one with it.

- Fiat Currency is a national currency not tied to commodities like gold or silver.

- Holders have the freedom to convert Digital Rupee into physical cash through commercial banks

- Its issuance follows the central bank’s financial policies.

- Block chain-based: CBDCs are transacted using blockchain-backed wallets.

- Backed by Central Bank: Unlike private cryptocurrencies, CBDCs are stable and trustworthy as they are backed by the central bank.

- Programmable Money: CBDCs can have programmable features, such as smart contracts, enabling automated, self-executing financial agreements.It can be programmed to expire, incentivizing consumers to use it by a specific date.

- Categories: The RBI has classified the digital rupee into two categories:

- General Purpose (Retail): Accessible to the public for regular use.

- Wholesale: For specific functions and accessible to financial institutions.

Significance of Central Bank Digital Currency

- Direct Bilateral Exchange: Countries could directly exchange digital currencies bilaterally without needing SWIFT or other settlement systems.

- Cost Reduction: CBDC can lower currency management costs by enabling real-time payments without inter-bank settlement.

- Cash Replacement in India: Given India’s high currency-to-GDP ratio, CBDC can reduce reliance on cash, minimising costs associated with printing, transporting, and storing paper currency.

- Additional Benefits:

-

- Reduced cash dependency.

- Higher seigniorage due to lower transaction costs.

- Lower settlement risks for transactions.

Check Out UPSC CSE Books From PW Store

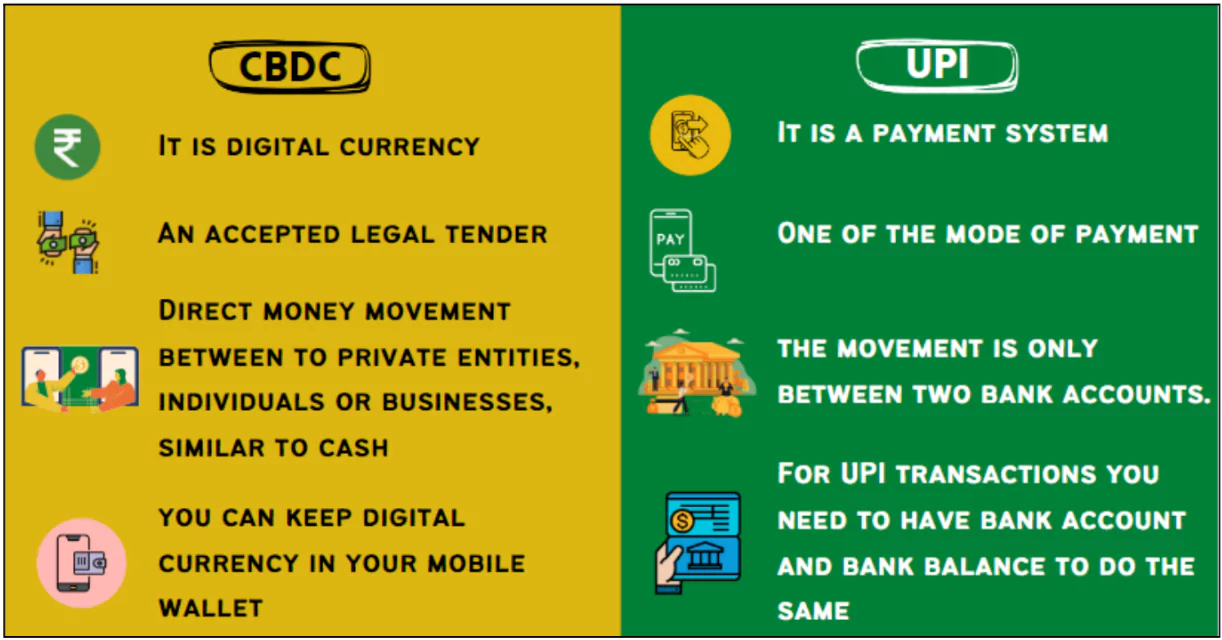

CBDC VS UPI

12 Nov 2024

12 Nov 2024

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program