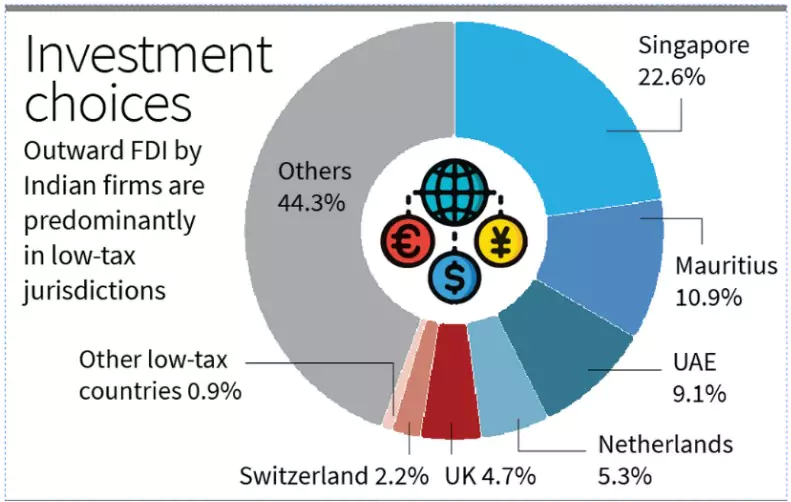

According to a RBI data, nearly 56% of India’s outward FDI in 2023–24 went to low-tax jurisdictions (commonly called tax havens) such as Singapore, Mauritius, UAE, the Netherlands, U.K., and Switzerland.

- In the first quarter of 2024–25, this figure rose to 63%.

- Foreign Direct Investment (FDI): Investment made by an individual/entity of one country into a business in another country, either by establishing business operations or acquiring business assets.

- Outward FDI: Investment made by Indian companies in foreign enterprises (through subsidiaries, joint ventures, or acquisitions) to expand globally.

- Tax Haven: A country/territory with very low or zero taxation, financial secrecy, and relaxed regulations, attracting foreign investors for tax efficiency.

- Examples: Mauritius, Singapore, Cayman Islands, Netherlands.

|

Outward FDI Trends

- Share of Tax Havens: In 2023–24, ₹1,946 crore of the total ₹3,488.5 crore outward FDI went to low-tax jurisdictions (56%).

- Key Destinations: Singapore (22.6%), Mauritius (10.9%), and UAE (9.1%) together accounted for more than 40% of total outward FDI.

Reasons Behind Preference for Tax Havens

- Intermediate Jurisdictions: Act as Special Purpose Vehicles (SPVs) for global expansion.

- Tax Efficiency: Lower tax liability in case of stake dilution or fund transfers.

- Investor Preference: Easier to attract global partners via Singapore/Mauritius than directly into India.

Regulatory Shield: Reduces exposure of Indian parent companies to domestic compliance/regulatory risks.

Regulatory Shield: Reduces exposure of Indian parent companies to domestic compliance/regulatory risks.- Ease of Operations: Flexible laws & fast fund movement compared to India.

- Fundraising Advantage: Capital raising is easier in such jurisdictions.

- Global Norm: Multinationals worldwide also use similar hubs.

Implications

Positive Implications

- Facilitates Global Expansion of Indian Firms

- Routing investments through Singapore or Mauritius allows Indian companies to set up Special Purpose Vehicles (SPVs) that serve as international hubs.

- Example: Infosys and Bharti Airtel use Singapore-based subsidiaries for Asia-Pacific operations.

- Helps in Joint Ventures & Access to Foreign Capital

- Tax havens with bilateral investment treaties and stable legal frameworks make it easier to attract foreign partners & venture capitalists.

- Example: Many Indo–U.S. or Indo–European joint ventures are structured through Singapore due to smoother legal processes.

- Provides Competitive Parity with Foreign Companies

- Since MNCs from other countries also use low-tax jurisdictions, Indian firms would be at a competitive disadvantage if they did not.

- Example: Global giants like Google and Apple use Ireland, Netherlands, Luxembourg, similarly Indian companies follow a similar path to remain globally competitive.

India’s Steps to Address Challenges of Tax Haven–Linked FDI

- Renegotiation of Tax Treaties: Double Taxation Avoidance Agreements (DTAAs) with countries like Mauritius (2016) and Singapore (2017) have been renegotiated to tighten capital gains exemptions.

- General Anti-Avoidance Rule (GAAR) – 2017: Introduced to check tax avoidance through complex arrangements and ensure fair tax practices.

- Transparency Mechanisms: Adoption of the OECD’s Common Reporting Standard (CRS) to improve information exchange.

- Profit Shifting Controls: Implementation of the OECD’s Base Erosion and Profit Shifting (BEPS) Action Plan to reduce artificial profit transfers.

- Global Minimum Tax: Adoption of OECD’s Pillar 2 initiative to ensure a minimum effective tax rate on multinational enterprises.

- SEBI Regulations on Round-Tripping: SEBI has tightened norms for Foreign Portfolio Investors (FPIs), especially from Mauritius, restricting opacity in beneficial ownership.

- Black Money (Undisclosed Foreign Income & Assets) Act, 2015: Provides for strict penalties & prosecution for undisclosed foreign assets; Allows confiscation of assets and imprisonment up to 10 years.

|

Concerns

- Profit Shifting and Tax Base Erosion

- By booking profits in Mauritius or Singapore subsidiaries, Indian firms minimise domestic tax liability, reducing India’s corporate tax revenues.

- Example: Past misuse of the India–Mauritius Double Taxation Avoidance Agreement (DTAA) for “round-tripping” investments.

- Regulatory Arbitrage and Weak Oversight

- Firms exploit gaps between Indian rules and foreign jurisdictions, making it harder for Indian regulators (RBI, SEBI, ED) to monitor flows.

- Example: PMLA and ED cases often involve complex layering through overseas shell entities.

- Tariff Impacts & Value Addition Abroad

- With U.S. tariffs on Indian exports, companies may relocate part of their manufacturing or processing abroad via these SPVs to bypass tariffs.

- Implication: Loss of domestic value addition and employment.

- Policy Challenge – Balancing Competitiveness with Tax Revenue

- Over-regulation may deter global competitiveness; under-regulation risks loss of tax income & illicit flows.

- Example: Debate over GAAR (General Anti-Avoidance Rules) and India’s renegotiation of tax treaties with Mauritius, Singapore, and Cyprus to plug misuse.

16 Sep 2025

16 Sep 2025

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program