Context:

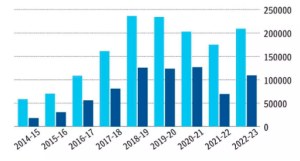

Banks have written off bad loans worth ₹14.56 lakh crore in the last nine financial years starting 2014-15.

More on News

Current Status of Loan Write-off in India:

- Total Loan written off: ₹14.56 lakh crore

- Loans Written-off by Category (Large Industries and Services): ₹7,40,968 crore

- Recovery in Written-off Loans by Scheduled Commercial Bank (SCBs):

| Period |

Recovery Amount (₹ crore) |

| April 2014 – March 2023 |

₹2,04,668 crore |

- Net write-off loans by public sector banks:

| Financial Year |

Net Write off In crore |

| FY18 |

1.18 lac |

| FY22 |

0.91 lac |

| FY23 |

0.84 lac |

- Net write-off loans by private sector banks: ₹73,803 crore (RBI provisional data) in FY23

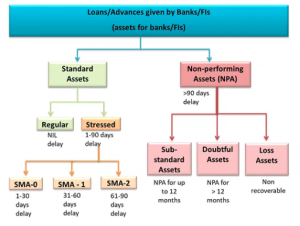

About Bad Loan and NPA:

- Bad Loan: A bad loan is that which has not been ‘serviced’ for a certain period.

- Servicing a loan is paying back the interest and a small part of the principal — depending on the agreement between bank and borrower.

- Non-Performing Asset (NPA):

- All advances given by banks are termed “assets”, as they generate income for the bank by way of interest or installments.

- However, a loan turns bad if the interest or installment remains unpaid even after the due date.

- A loan becomes an NPA when the principal or interest payment remains overdue for 90 days.

- For agriculture, if principle and interest is not paid for two cropping seasons, the loan is classified as NPA.

- Classifications of NPA:

Substandard Assets: Assets that have remained NPA for a period less than or equal to 12 months.

Substandard Assets: Assets that have remained NPA for a period less than or equal to 12 months.- Doubtful Assets: An asset remained in the substandard category for a period of 12 months.

- Loss Assets : An asset which is identified as a loss by the bank but not written off yet

- Additional Terms:

- Gross Non-Performing Assets (GNPA): It is the summation of all the loans that have defaulted by individuals from financial institutions.

- GNPA ratio is defined as a percentage of GNPA with total assets.

- Net Non-Performing Assets (NNPAs): It is calculated by subtracting provision for doubtful debt maintained by respective banks from GNPAs.

- The NNPAs ratio is defined as a percentage of NNPA with respect to total assets.

What is a loan write-off?

- A loan write-off occurs when a lender removes a loan from its books, no longer considering it as an asset due to borrower default.

- Tax Liability Reduction: Writing off loans decreases the bank’s tax liability as the written-off amount is subtracted from profits.

Status of NPA:

- In financial year 2022, public sector banks in India reported a total of over 5.4 trillion Indian rupees in gross non-performing assets (NPA).

- This was a decrease from the 7.3 trillion Indian rupees in 2019.

- In contrast, private sector banks reported a decrease from two trillion Indian rupees to 1.8 trillion Indian rupees in financial year 2022 in gross NPAs.

Factors Behind the Surge in NPAs:

- Economic Factors Leading to NPAs:

- Optimistic Economic Outlook: Many bad loans emerged during 2006-2008, a period of robust economic growth.

- This led to riskier lending decisions without proper due diligence.

- Global Economic Slowdown: Strong global growth pre-2008 Global Financial Crisis (GFC) was followed by a broader economic slowdown, affecting India too.

Structural Economic Inefficiencies: Project delays, cost overruns, and regulatory processes create inefficiencies that contribute to NPA generation.

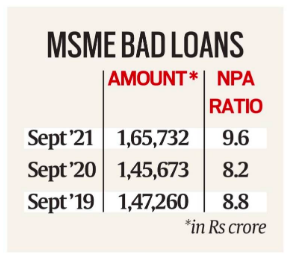

Structural Economic Inefficiencies: Project delays, cost overruns, and regulatory processes create inefficiencies that contribute to NPA generation.- Increased NPAs in MSMEs: Gross NPAs of MSMEs rose by Rs 20,000 crore to Rs 1,65,732 crore as of September 2021 from Rs 1,45,673 crore in September 2020.

- NPA under Pradhan Mantri MUDRA Yojana:

- The Micro Units Development & Refinance Agency (MUDRA) was launched on April 8, 2015 to provide loans up to Rs 10 lakh to non-corporate, non-farm, small and micro enterprises.

- Bad loans under the MUDRA Yojana for all banks is 3.38 per cent of the total disbursements.

- Structural Reasons:

- Lack of Identification: Lack of continuous monitoring in regulation resulted in evergreening loans instead of restructuring, delaying prompt action due to the inability to identify assets quickly.

- Loss of Interest from Promoters and Banks: When project delays depleted promoters’ equity, they lost interest. This led to project restructuring delay or banker abandonment, resulting in “zombie” projects.

- Weak Corporate Governance: Poor board quality with regard to due diligence, transparency, and accountability processes resulted in poor decision-making and ineffective credit utilization.

- Other Reasons:

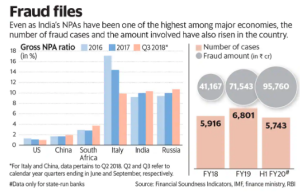

- Promoter Fraud: Fraud cases within public sector banks are on the rise, though smaller compared to overall NPAs. Lack of appropriate action against culprits might have led to fraudulent behavior.

Manipulation of Restructuring: Before the Insolvency and Bankruptcy Code, promoters had significant influence on restructuring.

Manipulation of Restructuring: Before the Insolvency and Bankruptcy Code, promoters had significant influence on restructuring.

- Promoters could convert bank lending to equity, benefiting from gains while shifting losses to banks.

How NPAs affect banks?

- Financial Performance: NPAs result in uncollected loan principal and interest, causing financial losses for banks. This affects their revenue and overall profitability.

- Capital Base: Banks need to set aside provisions for NPAs, eroding their capital base. This can challenge their ability to meet regulatory capital requirements.

- Liquidity Strain: Setting aside funds as provisions for NPAs affects banks’ liquidity, limiting their lending capacity and credit availability in the economy.

- The lack of liquidity prevents banks from lending and it may slow down the economy leading to unemployment, inflation, bear market, etc.

- High Interest Rate: To maintain their profit margins, banks will be forced to increase interest rates which again hurt the economy.

Laws and Provisions related to NPAs:

- The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002: It allows banks and financial institutions to seize collateral and sell them to recover dues without court intervention.

- Insolvency and Bankruptcy Code (IBC), 2016: It Offers a framework for time-bound resolution of stressed assets and supports creditors.

- Establishes National Company Law Tribunal (NCLT) and Insolvency and Bankruptcy Board of India (IBBI) to oversee the process.

- Bad Banks (2017): A bad bank separates risky and non-performing assets from a financial institution. It is also known as Asset Management Company (AMC).

- Former Interim Finance Minister introduced the idea of National ARC on the recommendation of the Sunil Mehta-led Committee.

- India’s first ever bad bank is National Asset Reconstruction Ltd (NARC). It purchases bad loans from banks, and sells them to distressed debt buyers.

- It is majorly controlled by PSBs, to acquire stressed loan assets above Rs 500 crore each amounting to about Rs 2 lakh crore in phases.

- India Debt Resolution Company Ltd (IDRCL) as an ARC sells stressed assets in the market.

- Prompt Corrective Action Framework:

- RBI launched PCA in 2002 for early intervention in struggling banks.

- Aim: To monitor and assist banks facing undercapitalization due to poor asset quality or loss of profitability.

- 2017 Review: The framework was reassessed in 2017 based on recommendations from the Financial Stability and Development Council and the Financial Sector Legislative Reforms Commission.

- Parameters include:

- Capital to Risk Weighted Assets Ratio (CRAR)

- Net Non-Performing Assets (NPA)

- Return on Assets (RoA)

- Gross NPAs of PSBs have declined to ₹4.28 lakh crore as on March 31, 2023 from ₹8.96 lakh crore as on March 31, 2018.

Way Forward:

- Time-Bound Resolution: Introduce a sunset clause for resolution through Bad Banks to ensure timely action.

- Asset Maintenance: Establish a suitable mechanism within Bad Banks to fund the maintenance of asset quality during the resolution process.

- Strengthened Resolution Oversight: Set up more panels similar to the one by Indian Banks’ Association (IBA) to oversee resolution plans.

- IBA has set up a six member panel to oversee resolution plans of lead lenders.

- Swift Recapitalization: Infuse additional capital into banks in a single installment to expedite recapitalization.

- Transparency: Continue transparent NPA recognition to maintain accurate data on bad loans.

- CIBIL Score: Utilize CIBIL scores to assess loan eligibility, ensuring responsible lending.

- Defaulters’ Information Circulation: Actively share information about defaulters to prevent them from obtaining further loans.

- Alternative Dispute Resolution Mechanisms: Promote the use of Debt Recovery Tribunals and Lok Adalats for quicker settlements.

News Source: The Hindubisinessline

8 Aug 2023

8 Aug 2023

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program