The Reserve Bank of India (RBI) has released the final guidelines for self-regulatory organizations (SROs) in the fintech sector.

About Self-regulatory organizations (SROs)

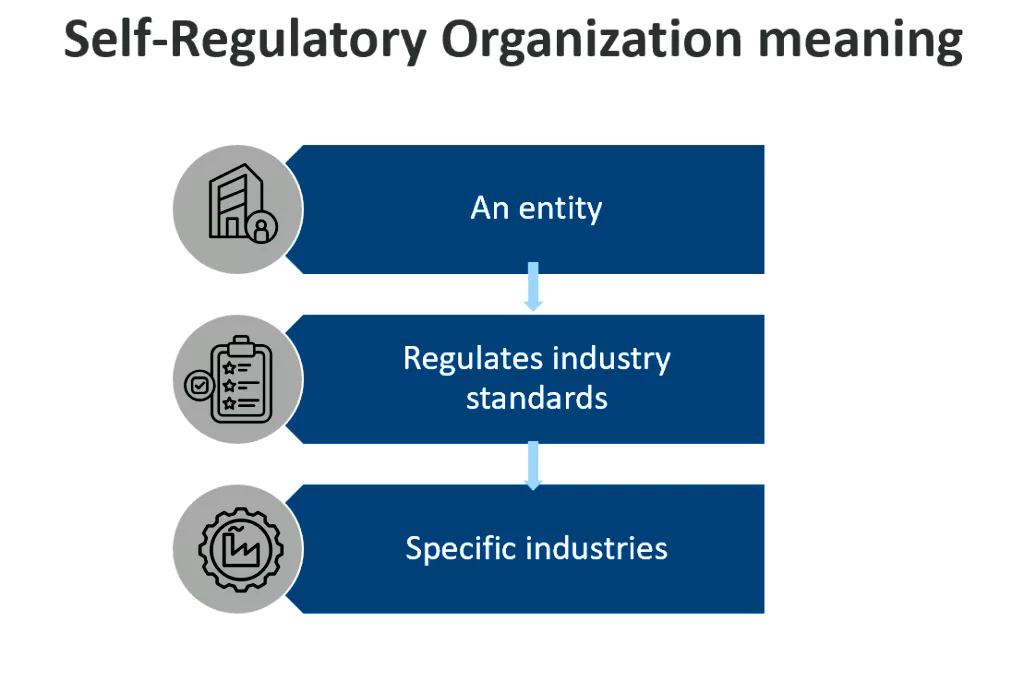

An Self-regulatory organizations (SROs) is a non- governmental organization that has regulatory power over an industry or profession.

- It sets rules and standards for entities in the industry by collaborating with all stakeholders.

- Objective: The main aim of this body is to protect customers, promote ethics, equality and participants in the ecosystem.

Enroll now for UPSC Online Course

-

Function

- Regulatory Authority: It can regulate in place of or alongside government regulation.

- Self regulatory process uses impartial mechanisms for its administration.

- All members operate in disciplined way due to impartial mechanism and accept the penal actions.

- Source of Authority: Its regulatory power is independent of the government grants.

-

How can an entity become an Self-regulatory organization?

- Apply to RBI: All interested entities have to apply to RBI for getting recognition as SROs.

- Letter of Recognition: Regulator issues a letter of recognition upon finding suitability of the entities.

Key highlights of the framework for Self-regulatory organizations in the Fintech sector

- Objective and Responsible Functioning: SRO-FTs are expected to function objectively and responsibly under the supervision of the RBI.

- Their primary goal is to ensure the healthy and sustainable development of the Fintech industry.

- Diverse Membership: The framework emphasizes the importance of SRO-FTs having a membership that broadly reflects the Fintech sector.

- This includes entities currently regulated by the RBI, like NBFC-account aggregators (NBFC-AAs) and P2P lending platforms, and non-bank members.

- Focus on User Protection: SRO-FTs are obligated to address instances of user harm, such as fraud, mis-selling of financial products, and unauthorized transactions.

- Multiple SROs Allowed: The RBI may permit multiple SROs within the fintech sector.

- Membership Flexibility: Fintech companies may join more than one SRO and are encouraged to participate in at least one.

- Establishment of Surveillance mechanisms: The framework emphasizes deployment of Surveillance mechanisms for detecting exceptions, while maintaining confidentiality and collecting important data.

- There is a provision of cautioning, reprimanding, counselling, or even expulsion from the SRO in case of violation of rules and regulation.

- A reasonable penalty can also be imposed.

- Structured frameworks for monitoring: This framework encourages SROs to establish a framework for monitoring fintech activities and ensuring its compliance with regulatory standards.

- Dispute resolution framework: SROs are required to establish a dispute resolution framework for its members within the Fintech industry.

- In addition to it, this body is responsible for Proactively addressing industry-wide concerns beyond individual member interests.

- Representation of the interest: SROs are responsible for representing the interests of its members when interacting with the RBI.

- Along with it, it has to Keep the RBI updated on fintech developments.

- It is responsible for Collecting and sharing data with the RBI to aid in policy making.

- SROs are to report regulatory violations and systemic issues within the sector to the RBI.

Criteria for SROs in Fintech

- Membership and Governance:

- Representative membership: Ensure a representative membership that reflects the entire sector, including regulated entities like account aggregators and P2P lenders, NBFCs, and non-regulated entities.

- Function independently and impartially, free from any single member’s influence.

- knowledge repository: Act as a knowledge repository and avoid conflicts of interest.

- Allow fintech firms to participate in multiple SROs if needed.

- Structure:

- Non-profit Structure: SRO-FTs must be established as not-for-profit companies.

- Minimum Net Worth Requirement: SRO-FTs need to maintain a minimum net worth of Rs 2 crore within one year of being recognized by the RBI.

- Shareholding: Have diversified shareholding, with no single entity holding more than 10% of the shares.

Enroll now for UPSC Online Classes

| Feature |

Benefit |

Challenge |

| Objective Operation & Healthy Growth |

- Promotes responsible innovation within a stable regulatory environment.

- Encourages long-term, sustainable development in the fintech sector.

|

- Balancing innovation with regulatory compliance can be complex.

|

| Phased Regulatory Compliance |

- Provides a clear path for fintech companies to navigate regulations.

- Reduces uncertainty and helps companies prepare for future oversight.

|

- The specific timeline and requirements for phased compliance may not be immediately clear.

|

| Industry Standards and Best Practices |

- Establishes a common ground for ethical conduct across the fintech sector.

- Improves transparency, disclosure, and data privacy practices for consumers.

|

* Developing and enforcing consistent standards across a diverse sector can be challenging. |

| Representative Membership |

- Ensures all voices within the fintech sector are heard.

- Promotes inclusivity and addresses the needs of various segments.

|

- Reaching a consensus among different types of members on standards and regulations might be difficult.

|

| Independent Governance |

- Fosters trust and confidence in the SRO’s decision-making.

- Reduces the risk of undue influence from any single entity.

|

- Ensuring true independence from powerful members can be a challenge.

|

| Member Development and Conduct |

- Upskills the fintech workforce and promotes responsible business practices.

- Encourages a culture of compliance and consumer protection.

|

- Enforcing disciplinary actions against members may face resistance.

|

| Collaboration with Regulators |

- Creates a channel for open communication between the industry and regulators.

- Provides valuable insights for shaping regulations that are both innovative and consumer-centric.

|

- Building trust and a productive working relationship with regulators may take time.

|

31 May 2024

31 May 2024

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program