Books

18 Jan 2025

18 Jan 2025

The Reserve Bank of India (RBI) has announced the list of Non-Banking Financial Companies (NBFCs) in the Upper Layer (UL) under Scale Based Regulation (SBR) for the year 2024-25

The NBFC Upper Layer (UL) list for 2024-25 includes Tata Sons Private Ltd, Bajaj Finance Ltd, LIC Housing Finance Ltd, and Aditya Birla Finance Ltd, among others.

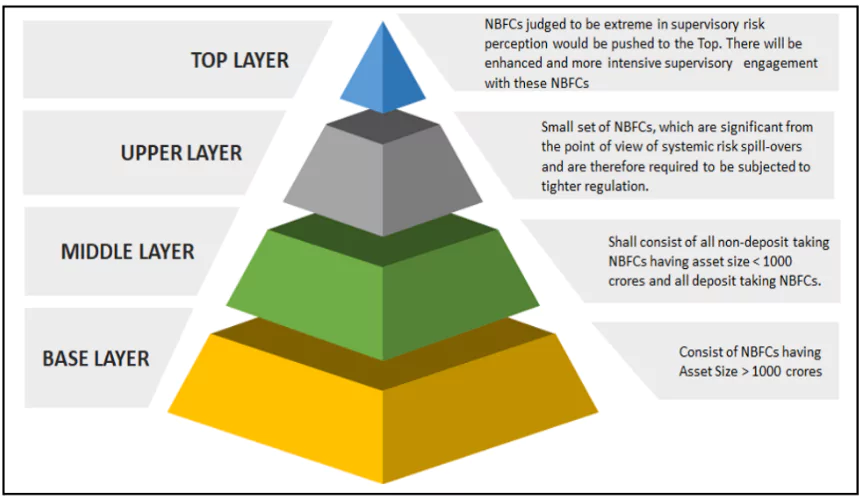

Categorization of NBFCs

Categorization of NBFCs

| Parameter | Banks | NBFCs |

| Demand Deposits | Can accept demand deposits | Cannot accept demand deposits |

| Payment and Settlement System (PSS) | Part of PSS; can issue cheques | Not part of PSS; cannot issue cheques |

| Deposit Insurance | Deposits insured by Deposit Insurance and Credit Guarantee Corporation | No deposit insurance facility available |

| Reserve Ratios (CRR, SLR) | Must maintain Reserve Ratios prescribed by RBI | Not required to maintain Reserve Ratios |

| Regulation Act | Regulated under Banking Regulation Act, 1949 | Regulated under Companies Act, 1956 |

| Foreign Direct Investment (FDI) | Up to 74% FDI allowed for private sector banks (49% under automatic route) | 100% FDI allowed |

Explore UPSC Test Series

.png)

Explore SRIJAN Prelims Crash Course

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program