A 10-year roadmap released by NITI Aayog projects that India’s $265-billion technology services sector could expand to $750–850 billion by 2035, contributing to the Viksit Bharat 2047 vision.

- The roadmap identifies five priority growth levers:

- Agentic AI,

- Software and Products,

- Digital Infrastructure,

- Innovation-led Engineering, and

- India-for-India solutions.

About the Technology Services Sector

- The technology services sector comprises IT services, business process management (BPM), digital engineering, cloud services, cybersecurity, AI solutions, and enterprise modernization support delivered to global and domestic clients.

- The sector includes software development, Enterprise Resource Planning (ERP) implementation, cloud migration, data analytics, AI model deployment, cybersecurity management, and digital transformation consulting.

- Key Features

- Export-Oriented Growth Model: The sector earns a significant share of revenue through exports, especially from the United States, and contributes nearly 7% of India’s GDP.

- Talent-Driven Competitive Advantage: India’s large pool of skilled, cost-effective engineers has enabled sustained global competitiveness and scalability.

- Transition Toward AI-Led Delivery: The industry is shifting from labour-arbitrage models to IP-led, AI-enabled, outcome-based service delivery frameworks.

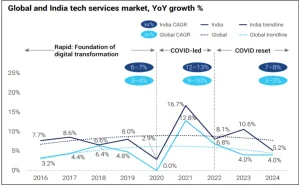

- Global Technology Services Landscape: The global technology services market is valued at approximately $1.3 trillion.

- It has witnessed phases of rapid digital adoption (2015–2020), COVID-driven acceleration (2020–2022), and post-pandemic AI-led disruption (2022–2024).

Current Status of the Technology Services Sector in India

- Market Share: India’s technology services industry currently generates about $265 billion annually and commands nearly 20% of the global market share.

- Growth in the Sector: The sector grew at 11–13% Compound Annual Growth Rate (CAGR) during the COVID surge but has moderated to 7–8% CAGR amid macroeconomic uncertainty, geopolitical tensions, visa restrictions, and early-stage AI disruption.

- Largest Share: Nearly 60% of exports are concentrated in the US market, making the industry sensitive to regulatory and economic changes in that region.

- Expanding Data Infra: India generates about 20% of global data, with data center capacity currently at 1.4 GW, expected to expand significantly over the next decade.

India’s Potential in the Technology Services Sector

- AI-Led Transformation Opportunity: Artificial Intelligence, especially GenAI and Agentic AI, is redefining service delivery models. India can evolve into a global hub for AI integration, model engineering, and governance.

- Expansion into Adjacent Markets: India can tap into adjacent global spend pools such as enterprise operations automation, SaaS products, digital infrastructure, AI-native platforms, and R&D engineering, with a combined Total Addressable Market (TAM) of nearly $14 trillion.

- Infrastructure and Data Advantage: India can position itself as a global AI infrastructure hub by expanding data center capacity from 1.4 GW to 10–12 GW by 2035 and increasing GPU-enabled infrastructure for AI workloads.

- Domestic Market Leverage (India-for-India Play): Rapid digital adoption in governance, UPI-based payments, health-tech, and multilingual AI platforms presents strong domestic growth opportunities.

- Innovation and IP Creation: By increasing R&D spending to 1–2% of revenues and building platform-based solutions, Indian firms can transition toward defensible intellectual property and higher value capture.

Government Initiatives to Boost the Technology Sector

- IndiaAI Mission (2024): The mission aims to build indigenous foundational AI models, create computer infrastructure, and establish an inclusive AI innovation ecosystem through the IndiaAI Innovation Centre.

- Research, Development and Innovation (RDI) Fund under ANRF: A ₹1 lakh crore fund provides concessional financing for high-risk deep-tech sectors such as semiconductors, quantum computing, and AI.

- National Deep Tech Startup Policy: The policy addresses funding, IP, and regulatory bottlenecks, providing extended benefits to commercialize deep-tech innovations.

- Digital India FutureLABS (2024): This initiative promotes next-generation electronics system design and fosters collaboration among academia, startups, and government for indigenous IP development.

- BharatGen (2024): BharatGen focuses on developing multimodal Large Language Models in Indian languages to enhance public service delivery and multilingual AI access.

Recommendations to Achieve India’s Potential

- Invest in Defensible IP and Platformization: Firms must allocate 1–2% of revenues to R&D and convert repeatable services into scalable, AI-native platforms.

- Reimagine Delivery Models with Agentic AI: The industry should transition to “human + agent + platform” models and shift toward outcome-linked commercial contracts.

- Diversify Markets and Vertical Focus: Companies must expand into different sectors like healthcare, defense, semiconductors, cybersecurity and different destinations such as Japan, the Middle East, and the domestic market,

- Scale AI-Focused Reskilling and Change Management: Workforce transformation should prioritize AI literacy, problem-solving, governance skills, and adaptive learning capabilities.

Conclusion

India’s technology services sector stands at an AI-driven inflection point; strategic innovation, infrastructure expansion, and IP-led growth can transform it into a $750–850 billion global leader by 2035.

14 Feb 2026

14 Feb 2026

.png)

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program