Books

16 Jan 2026

16 Jan 2026

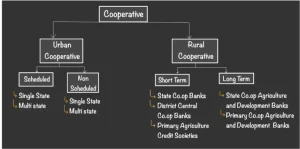

The Reserve Bank of India (RBI) has proposed reopening the licensing window for new urban co-operative banks (UCBs).

| Capital to Risk-Weighted Assets Ratio measures a bank’s capital adequacy by expressing its capital funds as a percentage of its risk-weighted assets. |

|---|

Eligibility: The RBI Proposal only for large co-operative credit societies with a minimum of 10 years of active operation and a good financial track record of at least 5 years.

Eligibility: The RBI Proposal only for large co-operative credit societies with a minimum of 10 years of active operation and a good financial track record of at least 5 years.

Tiered Regulatory Structure

|

|---|

Check Out UPSC CSE Books

Visit PW Store

| Aspect | Urban Cooperative Banks (UCBs) | Commercial Banks |

| Ownership | UCBS are owned by their members, who are both depositors and borrowers under the cooperative principle. | Commercial Banks are owned by shareholders, which may include the Government (in PSBs), institutions, or private investors. |

| Regulation | They are subject to dual regulation, where the RBI regulates banking operations, while State Governments/Central Government regulate management and incorporation. | They are regulated solely by the Reserve Bank of India (RBI) under the Banking Regulation Act, 1949. |

| Lending Focus | They Primarily lend to small traders, salaried persons, self-employed individuals, and MSMEs in urban and semi-urban areas. | They have a diversified lending portfolio, including large industries, infrastructure, MSMEs, agriculture, retail, and services sectors. |

| Voting Rights | Follows the “one member, one vote” principle, irrespective of the number of shares held. | Follow the “one share, one vote” principle, where voting rights are proportional to shareholding. |

.png)

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program