Books

16 Oct 2023

16 Oct 2023

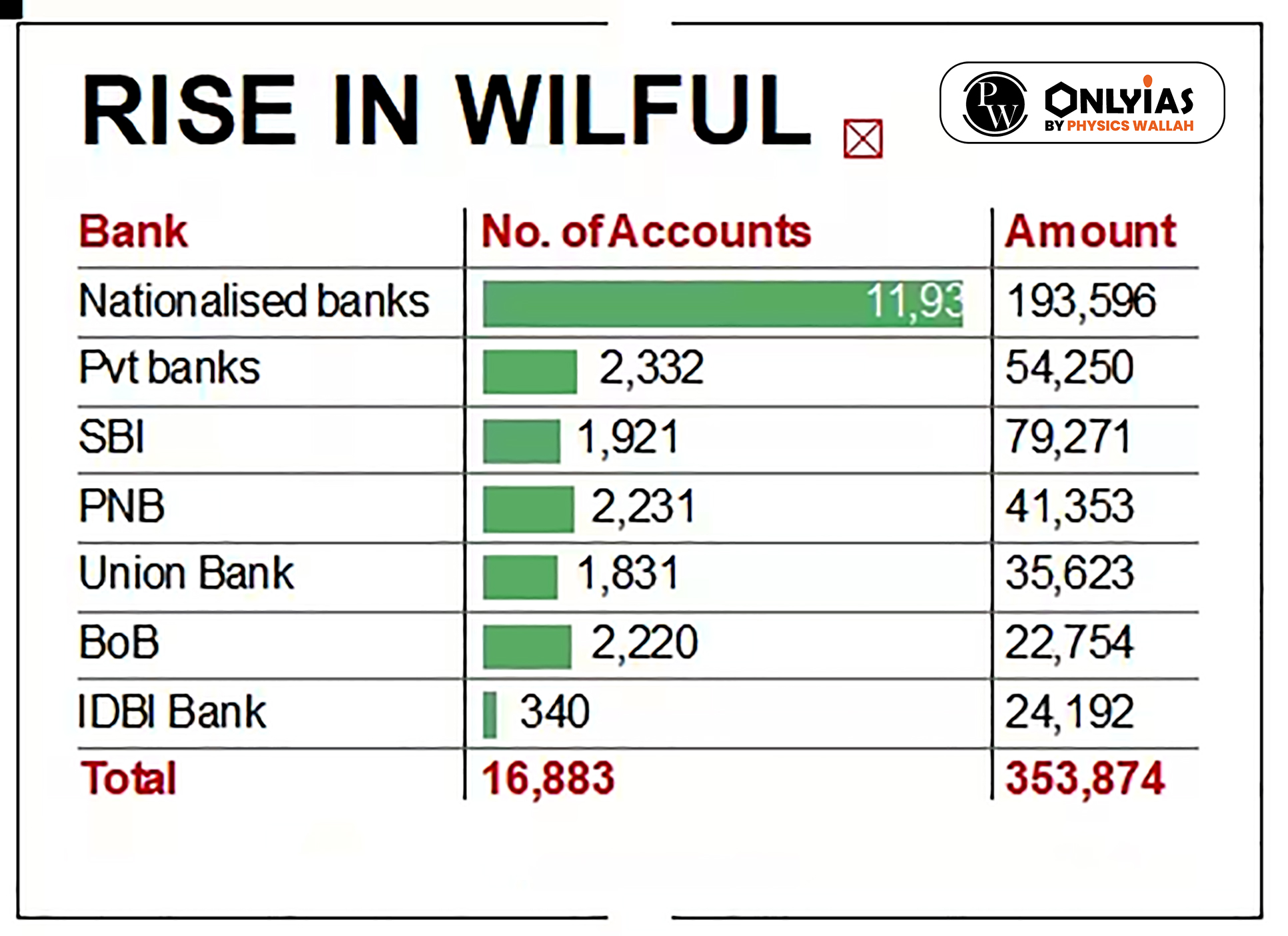

About Wilful Defaults: On September 21, the RBI proposed that lenders complete the process of classifying a borrower as a ‘wilful defaulter’ within six months of the account being declared as a non-performing asset (NPA).

RBI’s Position:On June 8, 2023, the RBI said in a circular that banks can undertake compromise settlements or technical write-offs regarding accounts categorized as wilful defaulters or fraud without prejudice to criminal proceedings against such debtors.

| Compromise Settlement refers to a negotiated settlement where a borrower offers to pay and the bank agrees to accept in full and final settlement of its dues an amount less than the total amount due to them under the loan contract. |

|---|

Source: Indian Express

.png)

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program