Books

December 1, 2023

December 1, 2023

Money is the commonly accepted medium of exchange. In economies with multiple individuals, money facilitates market transactions. Money facilitates exchanges by allowing individuals to sell their produce for money, which is then used to purchase necessary commodities. It serves various functions in a modern economy, including the facilitation of exchanges, market transactions, and facilitating the exchange of goods and services.

Money and Banking form an interdependent relationship. Once the money is in circulation, it is mainly the banking sector that gets involved in the transaction process.

Ever wondered why transactions are made in money?

The reason is simple. A person holding money can easily exchange it for any commodity or service that he or she might want.

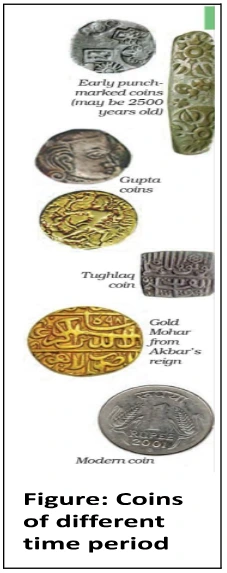

Money has served as a medium of exchange, with Indians using grains and cattle since ancient times. Metallic coins like gold, silver, and copper were introduced in the last century.

What roles do Modern Money and Banking play in today’s financial landscape?

Relationship between money and banking: Why do people hold money in deposits with banks?

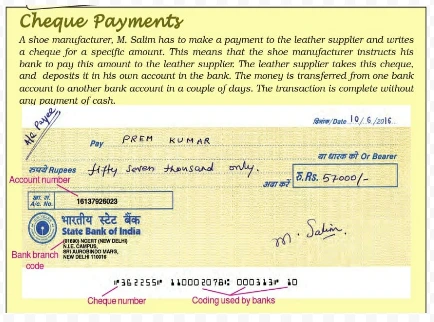

Cheque

Factors influencing Money Demand:

Money in a modern economy includes cash and bank deposits. These are created by the central bank and commercial banking system.

Let’s have a look at them in detail.

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program