Books

5 Apr 2024

5 Apr 2024

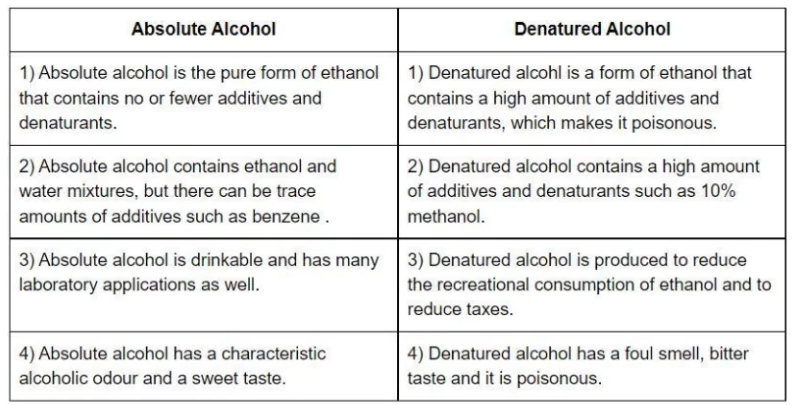

There is a hearing on whether states have the authority to levy excise duty on industrial alcohol by a 9-judge Bench of the Supreme Court.

Denaturation is the process of making industrial alcohol unsuitable for misuse or consumption.

Denaturation is the process of making industrial alcohol unsuitable for misuse or consumption.

| Must Read | |

| NCERT Notes For UPSC | UPSC Daily Current Affairs |

| UPSC Blogs | UPSC Daily Editorials |

| Daily Current Affairs Quiz | Daily Main Answer Writing |

| UPSC Mains Previous Year Papers | UPSC Test Series 2024 |

Explore UPSC Test Series

.png)

Explore SRIJAN Prelims Crash Course

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program