This quiz is based on UPSC STATIC SYLLABUS and is posted regularly on the PWOnlyIAS website for UPSC IAS.

To view Solutions, follow these instructions:

To Start quiz click on – ‘Start Quiz’

Solve all Questions.

Click on ‘Quiz Summary’

Click on ‘Finish Quiz’

Click on ‘View Questions’ button to see the all Explanations.

You have already completed the quiz before. Hence you can not start it again.

Quiz is loading...

You must sign in or sign up to start the quiz.

You have to finish following quiz, to start this quiz:

Results

0 of 5 questions answered correctly

Your time:

Time has elapsed

You have reached 0 of 0 points, (0)

Average score

Your score

Categories

Not categorized0%

Your result has been entered into leaderboard

Loading

maximum of 10 points

Pos.

Name

Entered on

Points

Result

Table is loading

No data available

1

2

3

4

5

Answered

Review

Question 1 of 5

1. Question

2 points

With reference to the Fiscal Responsibility and Budget Management (FRBM) Act, consider the following statements:

It deals with fiscal deficit, revenue deficit and public debt management.

The fiscal targets set by the act are legally binding on the government.

The act mandates the reduction of fiscal deficit to zero over a period of time.

Which of the statements given above is/are correct?

Correct

Ans: C

Exp:

Statement 1 is correct:The need for the Fiscal Responsibility and Budget Management (FRBM) Act in India arose from various economic and fiscal challenges that the country faced. The primary reasons for enacting the FRBM Act include:

Fiscal Imbalances: India was experiencing significant fiscal imbalances, with high levels of fiscal deficit and revenue deficit. These imbalances were leading to excessive government borrowing, which could have adverse effects on the economy, including inflation and interest rate volatility.

Public Debt Management: The increasing public debt burden was becoming a concern for the government. Effective debt management was necessary to ensure that public borrowing did not reach unsustainable levels, which could hinder long-term economic growth.

Statement 2 is correct: The fiscal targets set by the act are binding on the government, which means that the government is legally obligated to adhere to these targets.

Statement 3 is incorrect: The act seeks to eliminate the revenue deficit over a period of time and bring it to zero and not the fiscal deficit, signifying that the government should generate sufficient revenue to cover all its expenditures, excluding interest payments.

References: pwonlyias.com, NCERT Class 12th Economy: Chapter 5

Incorrect

Ans: C

Exp:

Statement 1 is correct:The need for the Fiscal Responsibility and Budget Management (FRBM) Act in India arose from various economic and fiscal challenges that the country faced. The primary reasons for enacting the FRBM Act include:

Fiscal Imbalances: India was experiencing significant fiscal imbalances, with high levels of fiscal deficit and revenue deficit. These imbalances were leading to excessive government borrowing, which could have adverse effects on the economy, including inflation and interest rate volatility.

Public Debt Management: The increasing public debt burden was becoming a concern for the government. Effective debt management was necessary to ensure that public borrowing did not reach unsustainable levels, which could hinder long-term economic growth.

Statement 2 is correct: The fiscal targets set by the act are binding on the government, which means that the government is legally obligated to adhere to these targets.

Statement 3 is incorrect: The act seeks to eliminate the revenue deficit over a period of time and bring it to zero and not the fiscal deficit, signifying that the government should generate sufficient revenue to cover all its expenditures, excluding interest payments.

References: pwonlyias.com, NCERT Class 12th Economy: Chapter 5

Question 2 of 5

2. Question

2 points

With reference to taxation, consider the following statements:

Tax buoyancy is the growth of tax revenues with growth in the income of the country.

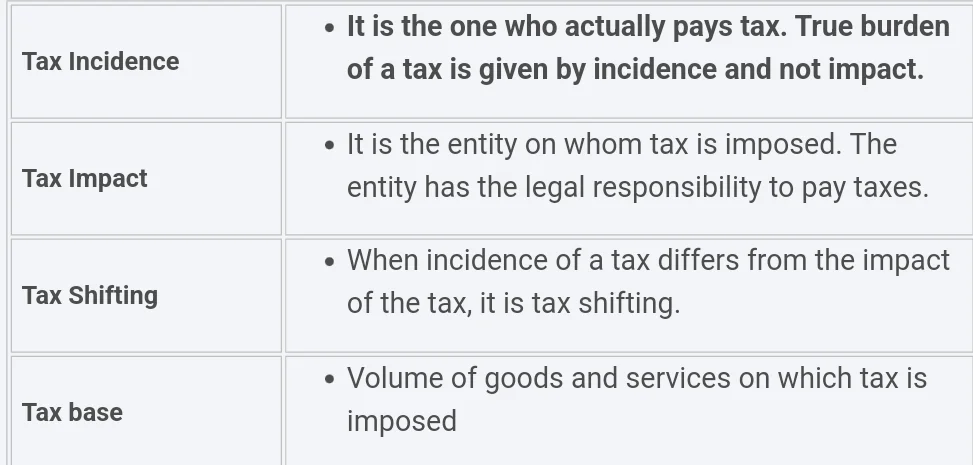

Tax shifting is a situation when the incidence of a tax differs from the impact of the tax.

Which of the statements given above is/are incorrect?

Correct

Ans: D

Exp:

Statement 1 is correct:The amount of tax income collected by the government and economic expansion are closely related. It is a basic reality that the government receives more tax income when the income or growth in the economy increases more quickly. The association between variations in the growth of tax revenues collected by the government and changes in GDP is explained by tax buoyancy. It speaks to how well tax revenue growth responds to changes in GDP. A tax’s revenue rises without the tax rate being raised when it is buoyant.

Statement 2 is correct: When the incidence of a tax differs from the impact of the tax, it is called tax shifting. Ex: Tax shifted by the companies to the consumer, while the governments intends it for the companies to pay them from their own revenues.

Statement 1 is correct:The amount of tax income collected by the government and economic expansion are closely related. It is a basic reality that the government receives more tax income when the income or growth in the economy increases more quickly. The association between variations in the growth of tax revenues collected by the government and changes in GDP is explained by tax buoyancy. It speaks to how well tax revenue growth responds to changes in GDP. A tax’s revenue rises without the tax rate being raised when it is buoyant.

Statement 2 is correct: When the incidence of a tax differs from the impact of the tax, it is called tax shifting. Ex: Tax shifted by the companies to the consumer, while the governments intends it for the companies to pay them from their own revenues.

With reference to Goods and Services Tax (GST), consider the following statements:

It is production-based taxation that is levied at the final consumption point.

The states are constitutionally empowered to impose Goods and services tax.

Lottery, Gambling and Betting are not taxable under the Goods and Services Tax (GST) Act, 2017.

How many of the above statements are correct?

Correct

Ans: A

Exp:

Goods and Services Tax (GST):

Consumption Tax: GST is essentially a consumption tax and is levied at the final consumption point. Hence, statement 1 is incorrect

Destination Principle: The principle used in GST taxation is the Destination Principle.

Levy On: It is levied on the value addition and provides set offs.

Avoid Cascading Effect: As a result, it avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

Collected On: It is collected on goods and services at each point of sale in the supply line.

In India, GST became a part by 101st Constitutional Amendment Act, 2016. This Amendment Act allows both the center and states to assess excise duty, Octroi tax, customs duty, service tax, entry tax, entertainment tax, etc., all substituted by the GST, making it a single indirect tax. Article 246A of the Indian Constitution states that States have power to tax goods and services. Hence, statement 2 is correct

Basic features of GST:

The Parliament and the state legislatures have concurrent powers to implement GST

It is a destination-based single tax.

Tax slabs are 0%, 5%, 12%, 18%, 28%

3 taxes are applicable within GST:

Centre levies the CENTRAL GST (CGST)

State levies STATE GST (SGST)

Centre levies INTEGRATED GST (IGST) on transactions

Parliament will compensate for any loss faced by the state.

Lottery, Gambling and Betting are also taxable under the Goods and Services Tax (GST) Act, 2017. Hence, statement 3 is incorrect

Consumption Tax: GST is essentially a consumption tax and is levied at the final consumption point. Hence, statement 1 is incorrect

Destination Principle: The principle used in GST taxation is the Destination Principle.

Levy On: It is levied on the value addition and provides set offs.

Avoid Cascading Effect: As a result, it avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

Collected On: It is collected on goods and services at each point of sale in the supply line.

In India, GST became a part by 101st Constitutional Amendment Act, 2016. This Amendment Act allows both the center and states to assess excise duty, Octroi tax, customs duty, service tax, entry tax, entertainment tax, etc., all substituted by the GST, making it a single indirect tax. Article 246A of the Indian Constitution states that States have power to tax goods and services. Hence, statement 2 is correct

Basic features of GST:

The Parliament and the state legislatures have concurrent powers to implement GST

It is a destination-based single tax.

Tax slabs are 0%, 5%, 12%, 18%, 28%

3 taxes are applicable within GST:

Centre levies the CENTRAL GST (CGST)

State levies STATE GST (SGST)

Centre levies INTEGRATED GST (IGST) on transactions

Parliament will compensate for any loss faced by the state.

Lottery, Gambling and Betting are also taxable under the Goods and Services Tax (GST) Act, 2017. Hence, statement 3 is incorrect

Which one of the following taxes is applicable to companies that show zero or no income?

Correct

Ans: D

Exp: To facilitate the taxation of ‘zero tax companies’-the companies which show zero or negligible income to avoid tax, despite showing hefty book profits the Minimum Alternate Tax was introduced.

Under this the companies are liable to pay a certain % of their book profit as tax. All companies in India, whether domestic or foreign, fall under this. According to income tax legislation, businesses are permitted to use a variety of deductions, exemptions, and provisions to determine their taxable income due to them, even when there is a sizable net profit recorded, the taxable profit may be zero.

But to get to the book profit after the MAT was implemented in 1996, the taxable profit must be adjusted for these deductions, transfers to reserves, depreciation, deferred tax, and other expenses.

Exp: To facilitate the taxation of ‘zero tax companies’-the companies which show zero or negligible income to avoid tax, despite showing hefty book profits the Minimum Alternate Tax was introduced.

Under this the companies are liable to pay a certain % of their book profit as tax. All companies in India, whether domestic or foreign, fall under this. According to income tax legislation, businesses are permitted to use a variety of deductions, exemptions, and provisions to determine their taxable income due to them, even when there is a sizable net profit recorded, the taxable profit may be zero.

But to get to the book profit after the MAT was implemented in 1996, the taxable profit must be adjusted for these deductions, transfers to reserves, depreciation, deferred tax, and other expenses.

With reference to Cess in India, consider the following statements:

Cess is an additional charge on a particular tax for an unspecified purpose.

The revenue from cess is kept in the Consolidated fund of India.

It cannot be levied on indirect taxes.

How many of the above statements are incorrect?

Correct

Ans: B

Exp: Cess is imposed over and above the tax for a specific predetermined purpose, like Swachh Bharat Cess. The surcharge is an additional charge on a particular tax. Hence, statement 1 is incorrect.

The revenue from cess is kept under the Consolidated Fund of India. Hence, statement 2 is correct.

Cess is not to be shared with the State and is resorted to only when there is a need to meet the particular expenditure for public welfare.

Cess is not a permanent source of revenue for the government, and it is discontinued when the purpose of levying it is fulfilled.

It can be levied on both indirect and direct taxes. Hence, statement 3 is incorrect.

Exp: Cess is imposed over and above the tax for a specific predetermined purpose, like Swachh Bharat Cess. The surcharge is an additional charge on a particular tax. Hence, statement 1 is incorrect.

The revenue from cess is kept under the Consolidated Fund of India. Hence, statement 2 is correct.

Cess is not to be shared with the State and is resorted to only when there is a need to meet the particular expenditure for public welfare.

Cess is not a permanent source of revenue for the government, and it is discontinued when the purpose of levying it is fulfilled.

It can be levied on both indirect and direct taxes. Hence, statement 3 is incorrect.

Fill The Required Details To Get Early Access Of Quality Content.

(Promise! We Will Not Spam You.)

Quick Revise Now !

AVAILABLE FOR DOWNLOAD SOON

UDAAN PRELIMS WALLAH

Comprehensive coverage with a concise format Integration of PYQ within the booklet Designed as per recent trends of Prelims questions हिंदी में भी उपलब्ध

Quick Revise Now ! UDAAN PRELIMS WALLAH

Comprehensive coverage with a concise format Integration of PYQ within the booklet Designed as per recent trends of Prelims questions हिंदी में भी उपलब्ध

<div class="new-fform">

</div>

Subscribe our Newsletter

Sign up now for our exclusive newsletter and be the first to know about our latest Initiatives, Quality Content, and much more.

Current Affairs

Current Affairs

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program

February 2, 2024

February 2, 2024