Books

2 Feb 2026

2 Feb 2026

The 2026-27 Union Budget represents a significant milestone in India’s economic journey, marking a shift towards a duty-based philosophy and strategic self-reliance in manufacturing.

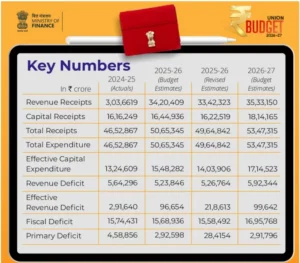

Revenue Receipts: These are government earnings that do not create repayment liabilities, comprising Tax Revenue (such as GST and Income Tax) and Non-Tax Revenue (including PSU dividends, user charges, fees, and fines).

Revenue Receipts: These are government earnings that do not create repayment liabilities, comprising Tax Revenue (such as GST and Income Tax) and Non-Tax Revenue (including PSU dividends, user charges, fees, and fines).

India’s Semiconductor Journey

|

|---|

Check Out UPSC CSE Books

Visit PW Store

| Mains Practice |

|---|

.png)

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program