Books

27 Nov 2023

27 Nov 2023

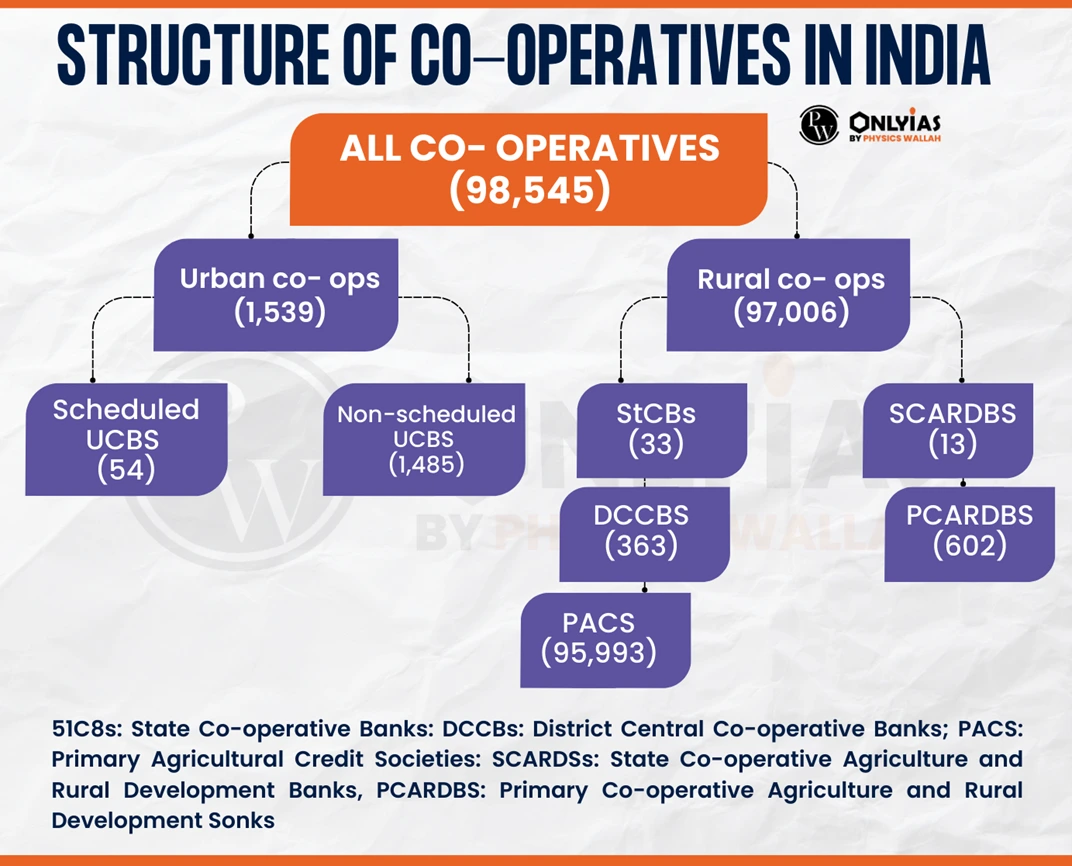

Context: Governance of Urban Cooperative Banks, Recently, the Reserve Bank of India (RBI) took over the board of Mumbai-based Abhyudaya Cooperative Bank Ltd for a year due to poor governance standards.

| Relevancy for Prelims: Cooperative Banks in India.

Relevancy for Mains: Challenges of Urban Cooperative Banks and Way Forward. |

|---|

Also Read: Banking Sector of India

Also Read: NPA in India

To thrive, Urban Cooperative Banks in India need better management, careful risk handling, and more ways to get money, focusing on growth and stability.

| Prelims Question (2021)

With reference to ‘Urban Cooperative banks’ in India consider the following statements: 1. They are supervised and regulated by local boards set up by the State Governments. 2. They can issue equity shares and preference shares. 3. They were brought under the purview of the Banking Regulation Act, 1949 through an Amendment in 1966. Which of the statements given above is/are correct? (a) 1 only (b) 2 and 3 only (c) 1 and 3 only (d) 1, 2 and 3 Ans: (b) |

|---|

Explore UPSC Test Series

.png)

Explore SRIJAN Prelims Crash Course

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program