Books

December 2, 2023

December 2, 2023

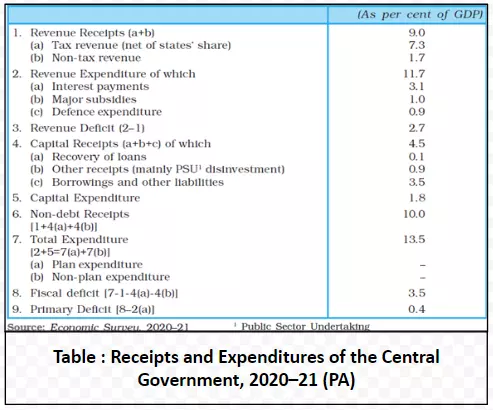

Revenue Receipts are defined as those receipts that do not create a claim on the government and, hence are termed as non-redeemable. They are broadly categorized into Tax Revenues and Non-Tax Revenues.

The taxation system is primarily categorized into two types:

Following are the capital receipts:

Understanding Revenue Expenditure: Plan vs. Non-Plan and Its Link to Government Receipts

Revenue Expenditure is classified into plan and Non-Plan Expenditure (Refer to Table ) as per budget documents:

Non-Plan Revenue Expenditure insights have an impact on government finances by directing governance and economic policies in relation to Government receipts.

Explore UPSC Test Series

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program