Books

December 5, 2023

December 5, 2023

Governments often step in to regulate prices when they are deemed too high or too low compared to desired levels. These interventions are analyzed within the framework of perfect competition to understand their impact on the affected markets.

|

POINTS TO PONDER The neo-liberal economic policy believes in market fundamentalism. These economists believe that the ‘invisible hand’ is the best and most efficient regulator of the market and demand for state non-intervention. Can you think of the need for the state and a welfare state in a fairly competitive market economy? |

|---|

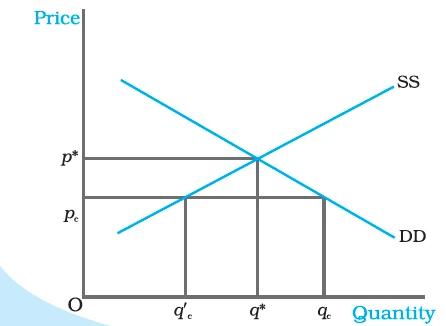

Effect of Price Ceiling in Wheat Market

The equilibrium price and quantity are p* and q* respectively. Imposition of price ceiling at pc gives rise to excess demand in the wheat market.

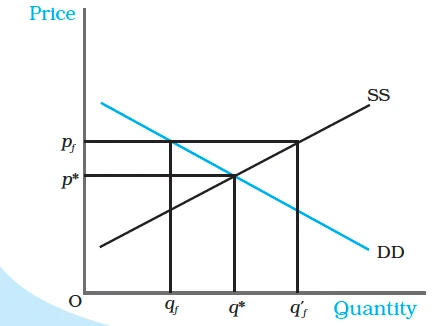

Effect of Price Floor on the Market for Goods

The market equilibrium is at (p*, q*). Imposition of price floor at pf gives rise to an excess supply.

|

Key points to remember about market equilibrium in a perfectly competitive market

|

|---|

Conclusion

Glossary

|

|---|

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program