Books

December 5, 2023

December 5, 2023

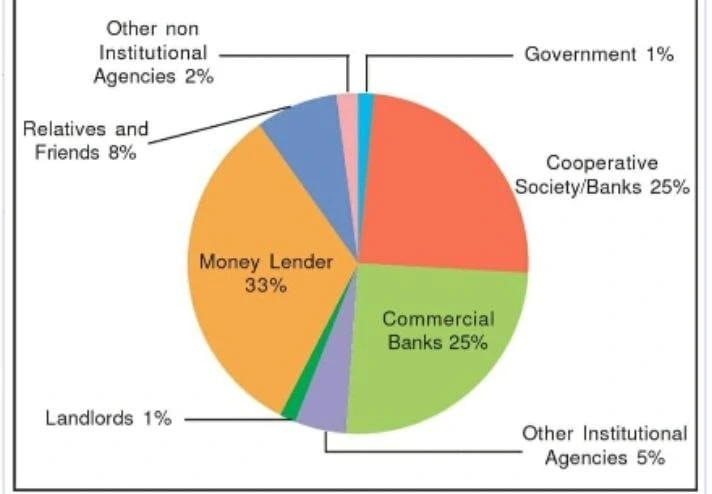

The various types of loans in India can be conveniently grouped as formal sector loans and informal sector loans. As shown in the figure, you can see the various sources of credit to rural households in India.

Sources of credit per Rs 1000 of Rural Households in India in 2012

Sources: Types of loans in India can be categorized in the form of moneylenders, traders, employers, relatives and friends, etc.

Characteristics of Informal Sectors Loan:

For these reasons, banks and cooperative societies need to lend more.

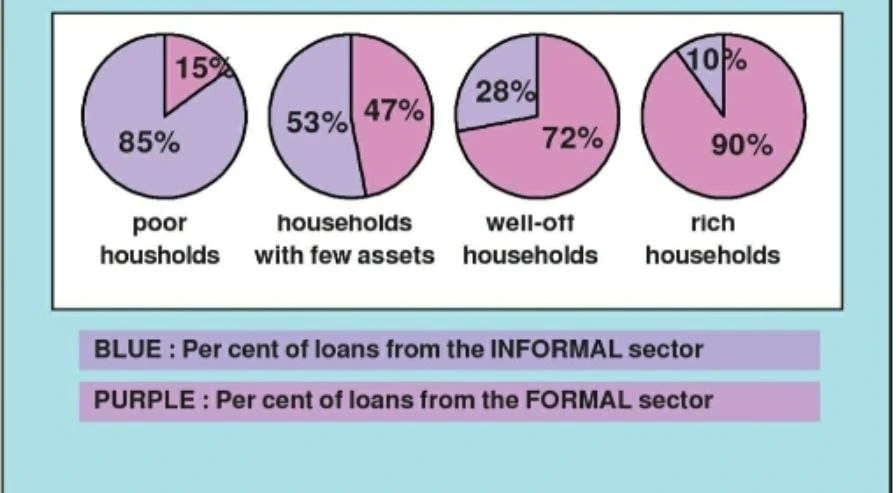

Urban Households Formal/Informal Loans

Definition: SHGs are organized groups of rural poor, particularly women, who themselves manage these groups by pooling their resources.

|

Grameen Bank of Bangladesh Bank of Bangladesh is one of the biggest success stories in reaching the poor to meet their credit needs at reasonable rates. Started in the 1970s as a small project, Grameen Bank in 2018 had over 9 million members in about 81,600 villages spread across Bangladesh. Almost all of the borrowers are women and belong to poorest sections of the society. |

|---|

Explore UPSC Test Series

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program