Udaan, Prahaar, Q&A Bank etc.

CA Magazines & Editorials

UPSC CSE : 2016

Answer:

| Approach:

Introduction

Body

Conclusion

|

Introduction:

Financial inclusion is defined by GoI as “the process of ensuring access to financial services and timely adequate credit when needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost”.

Dimensions of financial inclusion are bank penetration, credit penetration, deposit penetration for which Pradhan Mantri Jan-Dhan Yojana (PMJDY) is a major initiative. More than 46.25 crore beneficiaries have banked under PMJDY since inception.

Body:

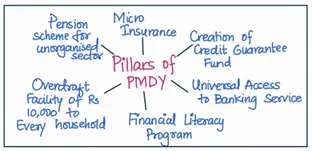

It ensures financial inclusion by:

But financial inclusion is not achieved simply by opening accounts. This can be seen as follows:

Conclusion:

PMJDY has achieved milestones and is truly a step in the right direction toward attaining financial inclusion. However further action is necessary to ensure that these accounts do not turn dormant in the time to come. A proactive effort by the government and other stakeholders holds the key to its success.

Join India’s trusted platform for expert guidance, quality content, proven success.

Learn anytime, anywhere.

India's leading UPSC coaching platform helping aspirants prepare for IAS, IPS, IFS and other Civil Services examinations with the best faculty and proven strategies.

<div class="new-fform">

</div>