Books

December 2, 2023

December 2, 2023

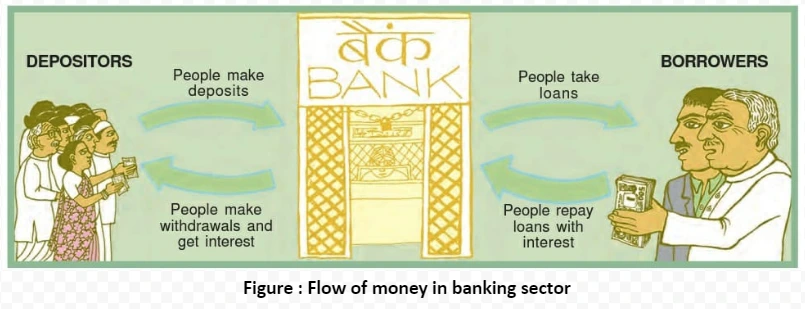

The Major function of the bank is accepting deposits from depositors and giving loans or credit to borrowers. Banks are able to perform these functions effectively with their ability to create money in the banking system.

Currency is generated by the RBI through the process of printing and backing it with the assurance of its value. This implies that the RBI has the capacity to produce any necessary amount of money. Have you considered the factors that discourage countries from simply printing money to fulfill their requirements, and what potential repercussions might arise from such a practice?

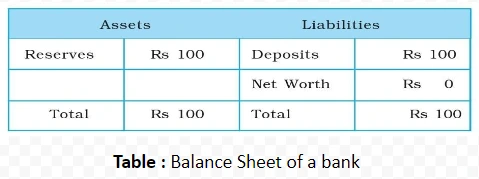

M1 = Currency + Deposits = 0 +100 =100

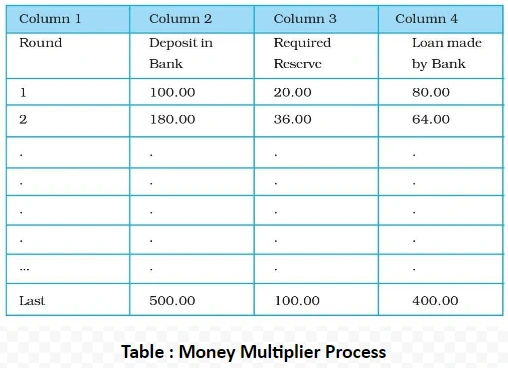

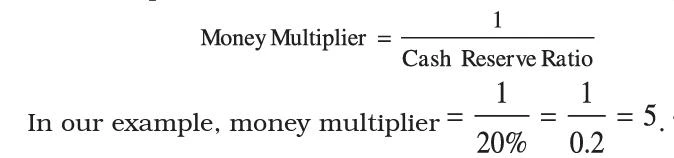

Cash Reserve Ratio (CRR) = Percentage of deposits which a bank must keep as cash reserves with the bank.

The Real interest rate is the difference between nominal interest rate and inflation. So the interest that we receive on our deposits is also influenced by inflation.

These terms play a pivotal role in shaping the credit landscape within the banking system.

Explore UPSC Test Series

Connect with our experts to get free counselling & start preparing

Books

Udaan (Prelims Wallah)

Prahaar (Mains Wallah)

Q&A Bank (Prelims & Mains)

Budget & Economic Survey

NCERT Wallah

Marks Booster

हिंदी माध्यम विशेष शृंखला

Current Affairs

Current Affairs

Monthly Current Wallah

Subject Wise Current Affairs

Editorial Analysis

Editorial PDFs

News of The Day

Download Our App

Download Our App

<div class="new-fform">

</div>

GS Foundation

GS Foundation Optional Course

Optional Course Combo Courses

Combo Courses Degree Program

Degree Program