Subject: GS 3: Economy

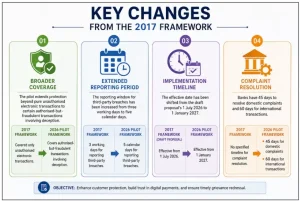

Context: The Reserve Bank of India (RBI) has introduced a pilot Digital Scam Compensation Framework by amending its 2017 guidelines on customer liability in unauthorised electronic banking transactions.

Best Online Coaching for UPSC

Key Highlights of the RBI Pilot Framework

Effective from 1 January 2027 for one year, the framework extends protection to victims of social engineering-based digital frauds, such as digital arrest scams, phishing, OTP theft, and coercion-induced payments, strengthening consumer confidence in India’s rapidly expanding digital payments ecosystem.

- Expanded Coverage: Extends compensation beyond unauthorised transactions to include Fraudulent Electronic Banking Transactions (EBTs) caused through deception, coercion, or stolen credentials.

- Compensation Mechanism: Individual victims suffering losses up to ₹50,000 are eligible for 85% reimbursement, subject to a maximum of ₹25,000, available once in a lifetime.

- Mandatory Reporting: Victims must report fraud through the National Cybercrime Helpline (1930) within five calendar days to claim compensation.

- Enhanced Protection: Reporting period for third-party unauthorised transactions has been increased from three working days to five calendar days.

- Shared Liability: Compensation will be jointly borne by the RBI, remitter bank, beneficiary bank, and the customer, reducing the burden on individual institutions.

- Pilot Implementation: The framework will operate as a one-year pilot during 2027, with possible expansion after evaluation.

India’s Earlier Such Initiatives

- RBI Customer Liability Framework (2017): Limited customer liability in unauthorised electronic banking transactions, primarily covering hacking and system breaches.

- Digital Payment Security Controls: Mandatory two-factor authentication, transaction alerts, UPI PIN verification, and risk-based authentication to secure electronic payments.

- National Cybercrime Reporting Portal & Helpline (1930): Enables prompt reporting, account freezing, and coordination among banks and law enforcement agencies.

- RBI Integrated Ombudsman Scheme (2021): Provides a unified grievance redressal mechanism for banking, NBFC, and digital payment complaints.

- Digital Payment Intelligence Platform (DPIP): AI-enabled platform for real-time fraud detection and coordinated fraud prevention across financial institutions.

- National Payments Corporation of India (NPCI) Safety Measures: Transaction limits, fraud monitoring, device binding, and real-time alerts across the Unified Payments Interface (UPI), Immediate Payment Service (IMPS), and other digital payment systems.

- Digital India & RBI Financial Literacy Initiatives: Promote cyber hygiene and awareness against phishing, OTP fraud, and social engineering attacks.

Global Such Actions:

- United Kingdom: The Authorised Push Payment (APP) Fraud Reimbursement Framework mandates reimbursement for eligible victims of bank transfer scams, with liability shared among payment service providers.

- European Union: The Revised Payment Services Directive (PSD2) mandates Strong Customer Authentication (SCA) and enhances consumer rights against unauthorised electronic payments.

- Singapore: The Monetary Authority of Singapore (MAS) introduced a Shared Responsibility Framework, allocating liability among banks, telecom operators, and consumers for phishing scams.

- Australia: The Scams Prevention Framework strengthens obligations on banks, telecom companies, and digital platforms to detect, prevent, and respond to scams.

- United States: Agencies such as the Consumer Financial Protection Bureau (CFPB) and banking regulators have strengthened consumer protection and reimbursement mechanisms for electronic fund transfer fraud under the Electronic Fund Transfer Act (EFTA).

|

Significance of RBI’s Digital Scam Compensation Pilot

- Strengthens Consumer Protection: Recognises that most modern cyber frauds rely on social engineering rather than direct hacking.

- Boosts Trust in Digital Payments: Reinforces confidence in UPI and electronic banking, supporting India’s digital economy.

- Promotes Timely Reporting: Encourages immediate reporting, improving fund recovery and fraud investigation.

- Supports Financial Inclusion: Provides a safety net for first-time victims, especially new digital payment users.

- Encourages Institutional Accountability: Incentivises banks and payment service providers to strengthen fraud prevention and customer awareness.

Challenges that need to be Addressed

- Limited Coverage: Excludes fraud losses exceeding ₹50,000 and restricts compensation to a single lifetime claim.

- Conditional Eligibility: Victims may lose eligibility if they ignore fraud warnings or fail to maintain updated contact details.

- Implementation Challenges: Requires robust grievance redressal, inter-bank coordination, and timely claim settlement.

- Rising Fraud Sophistication: AI-enabled phishing, impersonation, and cross-border cybercrime continue to evolve faster than existing safeguards.

Way Forward

- Strengthen the Compensation Framework: Expand coverage beyond ₹50,000, review the one-time lifetime compensation cap, and institutionalise the pilot based on performance evaluation.

- Enhance Fraud Prevention: Deploy AI-driven fraud detection, behavioural analytics, real-time transaction monitoring, and stronger cyber security infrastructure.

- Ensure Timely Grievance Redressal: Establish faster, technology-enabled claim settlement through seamless coordination among banks, the RBI, the National Payments Corporation of India (NPCI), and law enforcement agencies.

- Promote Inclusive Consumer Protection: Adopt a risk-based approach by providing enhanced safeguards for senior citizens, first-time digital users, and other vulnerable groups.

- Strengthen Digital Financial Literacy: Intensify nationwide awareness campaigns on phishing, OTP fraud, digital arrest scams, and other social engineering attacks.

- Foster Shared Accountability & Global Alignment: Clearly define responsibilities of banks, payment service providers, telecom operators, and customers, while aligning India’s framework with global best practices in digital payment security and consumer compensation.

Click to Know UPSC Coaching Centres in India

Conclusion

By combining strong preventive safeguards with a fair compensation mechanism, the RBI’s pilot marks a significant step towards a secure, trusted, and inclusive digital payments ecosystem, reinforcing public confidence in India’s rapidly expanding digital economy.

30 Jun 2026

30 Jun 2026