While the PM Surya Ghar: Muft Bijli Yojana has achieved a milestone of 40 lakh installations (adding over 12 GW capacity), the government’s target of reaching 75 lakh households by year-end faces a supply-chain bottleneck.

- This is due to the rising costs and limited availability of panels tied to the Domestic Content Requirement (DCR) mandate.

UPSC Coaching Classes

About the PM Surya Ghar Mandate & The Supply Gap: (UPSC CSE Prelims 2025)

- It is a rooftop solar scheme launched by the Government of India to promote the installation of solar power systems in residential households.

- The scheme aims to:

- Provide financial assistance (subsidy) for installing rooftop solar panels in households.

- Enable 1 crore households to generate their own clean electricity.

- Help households receive benefits equivalent to up to 300 units of free electricity per month through solar power generation and reduced electricity bills.

- Promote renewable energy adoption and reduce dependence on conventional sources of electricity.

- The Scheme Mandate: Under the PM Surya Ghar framework, it is mandatory to use DCR-compliant solar panels to qualify for central government subsidies.

-

- About DCR: Domestic Content Requirement (DCR) specifies that the solar panels deployed must be built using locally manufactured solar cells (the core semiconductor components that convert sunlight into electricity).

- The June 2026 Policy Trigger: Effective June 1, 2026, the Ministry of New and Renewable Energy mandated the use of solar cells listed under the Approved List of Models and Manufacturers (ALMM) List-II for eligible solar projects.

- Objective: To reduce dependence on imported solar photovoltaic cells and promote domestic manufacturing.

- However, rooftop solar consumers under the PM Surya Ghar: Muft Bijli Yojana who voluntarily forgo Central Financial Assistance (CFA) under the ‘Give It Up’ option are exempt from this requirement until March 31, 2027.

- The Structural Deficit: This policy expansion has exposed India’s industrial mismatch between panel assembly and cell core manufacturing:

- Solar Module (Panel) Assembly Capacity: ~60–65 GW per year.

- Solar Cell Manufacturing Capacity: Only ~30 GW per year.

- The Deficit: Because cell capacity is less than half of module capacity, India’s green energy sector has historically relied heavily on imported solar cells to bridge the gap.

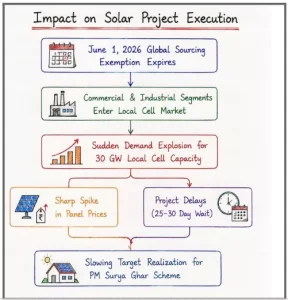

Impact on Solar Project Execution

- Project Delays: Ground-level vendors across states like Uttar Pradesh, Haryana, and Odisha report severe shortages. Major domestic manufacturers are operating at maximum capacity, causing a 25–30 day waiting period for panel procurement.

- Price Escalation: The sudden expansion of the local sourcing mandate to commercial and industrial projects sparked an aggressive demand surge, causing DCR-compliant module prices to rise sharply.

- Consumer Uncertainty: The supply crunch risks stalling momentum for residential consumers who have already received project approvals or made advance payments.

Significance of the Local Cell Mandate

- Reducing Import Dependency: The long-term objective of the DCR policy is to insulate India’s renewable energy sector from external supply shocks and heavy import reliance on dominant global suppliers.

- Strengthening Domestic Ecosystems: By guaranteeing a captive domestic market, the policy encourages large-scale private investment into setting up high-tech solar cell fabrication plants inside India.

- Aligning with Aatmanirbhar Bharat: The mandate ensures that the enormous fiscal subsidies disbursed under the PM Surya Ghar scheme directly fuel domestic manufacturing jobs and industrial GDP growth rather than leaking abroad.

Concerns and Implementation Challenges

- Target Realization Risk: With India adding roughly 45 GW of solar capacity annually, a restricted 30 GW domestic cell pipeline creates an immediate bottleneck that threatens the government’s year-end housing targets.

- Cost Overruns for Installers: Small and medium Distributed Renewable Energy (DRE) vendors operate on thin margins; sudden input price inflation impacts their viability and slows down rooftop solar adoption.

- Quality and Scalability Balance: Transitioning overnight to domestic sourcing before domestic manufacturing lines fully mature can lead to short-term compromises on cost competitiveness and technology scaling.

| Difference Between Solar Cells and Solar Modules |

| Feature |

Solar Cell |

Solar Module (Panel) |

| What It Is |

- The fundamental semiconductor unit (usually made of silicon) that converts light into electricity via the photovoltaic effect.

|

- An assembled structural framework containing a network of multiple interconnected solar cells.

|

| Manufacturing Complexity |

- Highly capital-intensive; requires advanced cleanroom technologies and chemical processing lines.

|

- Primarily involves assembly, soldering, encapsulation, and framing of cells into weatherproof structures.

|

| India’s Status |

- Experiencing a structural deficit (~30 GW capacity), leading to high historic import reliance.

|

- Highly self-sufficient (~60–65 GW capacity), capable of meeting domestic assembly demand.

|

Click to Know UPSC OnlyIAS Coaching Centres

Way Forward

- Fast-tracking Capacity Additions: The MNRE must work closely with domestic manufacturers to bring upcoming solar PV cell production units online ahead of schedule to ease the demand-supply friction.

- Dynamic Price Monitoring: The joint monitoring system led by REC Limited and the National Institute of Solar Energy (NISE) must actively curb artificial hoarding or predatory pricing by domestic cell suppliers during this transitional crunch.

- Calibrated Policy Phasing: For upcoming distributed solar projects (like agricultural pumps and residential rooftops), the government could consider a brief, tapered implementation window or graded import permissions until local cell capacity crosses the critical 50 GW threshold.

12 Jun 2026

12 Jun 2026